The cap rate calculator, alternatively called the capitalization rate calculator, is a tool for everyone interested in real estate. As the name suggests, it calculates the cap rate based on the value of the real estate property and the income from renting it. You can use it to decide whether a property's price is justified or determine the selling price of a property you own. In this article, you will learn how to calculate the cap rate, what is the cap rate formula, and how to understand the cap rate definition. You will also get some insight into the practical concept of the capitalization rate together with helpful advice. In the end, you will surely know what is a good cap rate.

Make sure to check out our real estate commission calculator as well! Besides, you may look at the rental property calculator which is an extended version of the cap rate calculator.

What is the cap rate definition?

Put simply, cap rate definition is the rate of return on a real estate investment property. In other words, it describes what part of your initial investment will return to you every year.

For example, imagine that you bought an apartment for $100,000, and the cap rate is 10%. It means that each year, 10% of the initial investment will return to you. As you can easily calculate, your net cash flow will be equal to zero after ten years, which means that you will actually start to make money on this investment from the eleventh year onwards.

What is the cap rate formula?

The description above makes it easy to figure out the cap rate formula by yourself. Basically, the cap rate is the ratio of net operating income (NOI) to property value or sales price.

cap rate = net operating income / property value

In other words, this ratio is a straightforward way to measure the relationship between the return generated by the property and its price. (For more information on ratios, check our ratio calculator).

Suppose you are a more advanced real estate investor. In that case, you can also include additional parameters: the vacancy rate (that is, during what percentage of the time does the property stay unoccupied) and the percentage of operating expenses (such costs as insurance, utilities, and maintenance).

It is important to note that operating expenses do not include mortgage payments, depreciation, or income taxes; therefore, the net income is the cash you earn before debt service and before income tax.

You can then use the following formula for the net income:

net income = (100 - operating expenses)[%] * (100 - vacancy rate)[%] * gross income

How to calculate the cap rate?

You can use the formulas mentioned above manually or calculate the cap rate with our cap rate calculator. To do it, follow these simple steps:

-

Begin with determining the property value – it can be, for example, its selling price. Let's say it is equal to $200,000.

-

Find out your gross rental income. It is simply the amount of money you get from your tenants each year. Let's say it is equal to $30,000 per year.

-

Determine the vacancy rate. Let's say that the property stays unoccupied for 2% of the time.

-

Decide on the percentage of operating expenses. Let's say you have to spend $500 monthly on costs – this is $6000 a year, which is equal to 20% of your gross income.

-

Use the following formula above to calculate the net rental income:

net income = (100 - 20)% * (100 - 2)% * $30,000 = 0.8 * 0.98 * $30,000 = $23,520 -

Lastly, divide the net income by the property value to obtain the cap rate:

cap rate = $23,520 / $200,000 = 11.76%

Capitalization rate application: selling a property

When do we need to calculate the cap rate? Imagine the following situation: you want to sell your property. You are not sure what the price is you should sell it at. The only thing you know is that your monthly operating income is $2,800, which is equivalent to $33,600 a year.

The best thing to do is to ask around for the cap rate. You are most likely to get this type of information from a commercial real estate agent. Let's say the average cap rate in your neighborhood is 9.7%.

To calculate the market value of your property, you simply have to divide the net income by the cap rate:

$33,600 / 9.7% = $33,600 / 0.097 = $346,392

This result is the value of your property. Of course, consider this as a rule of thumb – there might be other reasons for increasing or lowering the selling price. Nevertheless, this is an excellent point to start from.

How to evaluate your property with its capitalization rate?

Probably the best way to understand how applying the capitalization rate helps in property evaluation is to look at a real-world example. Let's say you are considering selling your house, and after some research, you see that investors are buying properties like yours at a 10 percent capitalization rate.

The 10 percent cap rate means a 10 percent profit on an investment. So, for instance, if you invest 1,000 dollars, you make 100 dollars which is a 10 percent return on investment. Placing it in a simple formula:

Rate of return = $100 profit / $1,000 investment = 10%

This is expressed in the context of property investment:

Cap rate = Annual net income / Value of the property

But what is the value of the investment if you have, let's say, $12,000 yearly net income on your property after receiving $1,000 monthly rents (or you find out that you could have such net income if you were to rent out your house)?

You probably already know how to get this number, but to see this with a mathematical expression, we need to rearrange the previous formula:

Value of the property = Annual net income / Cap rate

Value of the property = $12,000 / 0.1 = $120,000

That means that your house is worth $120,000.

How does a change in net income affect the value of a property?

Now, as you have more insight into property evaluation by cap rate, let's see what happens if there is a change in the local real estate market.

As a simple example, let's imagine that more and more tourists visit the area where your house is located because of the growing popularity of the sharing economy and Airbnb. As a result of the higher demand you decide to take this business opportunity, and you rent out your rooms with higher rent for shorter periods. Accordingly, your total net income in a year increases from $12,000 to $15,000. What happens with the value of your property in this situation?

Value = $15,000 / 0.1

The estimated price of your house rises to $150,000.

The above example is relatively straightforward: the higher the demand, the higher the prices. But what happens when there is a change in the capitalization rate? In the following section, you can get familiar with such a situation as well.

How does a change in cap rate affect the value of a property – the importance of interest rates for cap rate

One of the common external aspects that can alter the business environment is a change in interest rates. In this vein, let's consider a situation of hiking interest rates. In such a case, other types of investments that are more directly connected to interest rates (for example, corporate bonds) may become more attractive for investors than buying properties. It follows that investors are not satisfied with a 10 percent rate of return anymore, but they require, let's say, a 12 percent cap rate for real estate investment.

Value = $12,000 / 0.12 = $100,000

As you can see, at the time of increasing interest rates, your house became less valuable. Why? Because investors must pay less for your home to receive a higher rate of return after the same net income.

Let's assume the opposite situation: what happens when interest rates go down? In that case, the cap rates drop as well; thus, your house price rises.

What is the bottom line? Even if the rental prices are not affected, external circumstances in the economy can influence the property's market value through the capitalization rate.

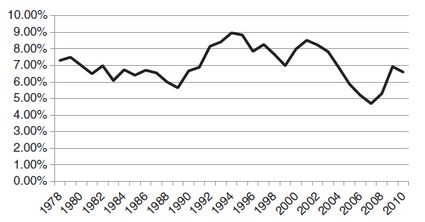

Cap rates and housing booms

Owning a house has traditionally been a part of the American dream. As the housing sector takes a considerable slice from the U.S. GDP, it is not surprising that a wide range of society tries to take advantage when house prices are going up. In such a time, politicians, bankers, investors, and ordinary home buyers mutually bolster the real estate market. The collective engagement in the housing business turned particularly forcible in the United States from the beginning of the 2000s when buying a house became an attractive way of investment. Most of us know or even experienced the disastrous effect of the 2008 financial crisis which was the culmination of the extended period of zealous rush in the real estate market.

But what happened to the capitalization rate during this time?

Apparently, policymakers and banks played a crucial role in the housing boom by providing easy access for mortgage loans. PLease check out our mortgage calculator to understand more. As a result of innovations in the financial sector and low interest rates, mortgage loans flooded the housing market. The increasing demand with easy credits generated house price inflation, and capitalization rates fell to unprecedented levels.

In 2002, cap rates were around the range of 8.5-9 percent, which is close to the long-run average. However, after several years of steady fall, cap rates reached a historically low 6.5 percent level. The steep drop in cap rates verified the presence of a speculative bubble on the housing market.

How to calculate cap rate when you buy a house – what is a good cap rate?

Using the capitalization rate to estimate the price of your property requires precise information about cap rates in the area where you would like to buy the house. You may turn to appraisers, commercial brokers, or independent services for advice to gain the most accurate data. You can also find some guidelines on the Internet, for example, at .

However, if you are considering buying a house or an apartment without a precise concept, you will most probably find plenty of offers on the market. If you quickly sort out the ones which are not worth considering, you can save a lot of time.

As a starting point, it is worth knowing that the historical cap rates are around 8-12 percent, which may serve as a handy guideline. As a rule of thumb, you may use a 10 percent cap rate as a basic and casual screening practice, which is super easy to compute without any calculator: you just need to add a zero to the potential net income.

It is not the way on which you should ever base your final decision, though it can give you a quick initial idea if it's worth spending more time to check the offer in detail. If you see a flat for sale for 500,000 dollars and you know that rents for such a flat in that area are roughly 1,000 dollars per month, which is 12,000 dollars in a year, you already know that it is better to pass it over (should be around to $120,000).

Property evaluation techniques

There are three conventional ways of property valuation, and they all rely on the basis of comparison.

1. Sales comparison techniques

In this case, the estimation is based on the price of similar properties on the market.

2. Replacement cost methods

In this approach, the guideline is the estimation of the expenses for constructing a similar property taking into account the depreciation rates and land values.

3. Income techniques

Evaluations of properties by their income streams or yields are related to income techniques. The core of this technique is the estimation of the capacity to generate economic benefit during the property's lifetime.

Property evaluation ratios

There are multiple financial ratios that can support the decision-making when you are about to buy or sell a property. Among them, the capitalization rate is probably the most popular ratio; however, there are others that also can give you practical guidance.

Besides the capitalization rate, the four other essential ratios are the following:

-

The cash return on investment (Cash ROI)

The cash return on investment, often called the cash-on-cash return, is the ratio of the remaining cash after debt repayment to the invested capital. The cash-on-cash ratio and the capitalization rate have an important distinction: the cash ROI is computed after debt service, while the cap rate doesn't consider the debt service.

Cash-on-cash ratio = remaining net income after debt service / invested cash -

The total return on investment (Total ROI)

The total return on investment is comparable to the cash-on-cash ratio, with one crucial difference: it represents the fraction of return that is not cash, namely the principal reduction. Putting it differently, it considers the principal portion of the loan payment in the equation. Therefore the total ROI is the ratio of the remaining cash after debt service plus principal payments to the invested capital:

The total return on investment = (remaining cash after debt service + principal reduction) / invested cash -

The debt service coverage ratio (DSCR)

The debt service coverage ratio, also known as the debt service ratio, evaluates the relation of the amount of cash available to service the debt payments, which is the net operating income, to the required debt payment.

The debt service coverage ratio = net operating income / debt payment -

The gross rent multiplier (GRM)

The gross rent multiplier, or GRM, signifies the relationship between the total purchase price of a property and its gross scheduled income. Therefore, it is the ratio of price to income.

Gross Rent Multiplier = purchase price / gross scheduled income

As the above ratios consider further financial dimensions of the property investment, they are helpful substitutes or complements for the cap rate.

Limitations of the capitalization rate

The application of capitalization rate during property evaluation is undoubtedly a convenient device; however, employing cap rates alone or inappropriately using them can lead to a severe flaw in your decision-making. As mentioned before, the cap rate doesn't account for debt payment in contrast to other debt-related ratios. Because mortgage loans often finance house purchases, a cash-on-cash investment ratio may give you a better guideline.

Besides, there are cases when the cap rate simply doesn't apply. For instance, when your target is a short-term property investment, the cap rate is not a proper tool to use since these types of investments do not generate income from rent.

Also, as demonstrated, the interest rate environment can affect the cap rates, which can be considered an external factor, not driven by the real estate market but caused by the Federal Reserve's monetary policy. Since the 2008 financial crisis, the policy rate was at the zero-level bound for several years, which pushed other interest rates to an unusually low range as well. Accordingly, cap rates dropped, which induced house price growth, especially in New York and San Francisco.

Using cap rates correctly, with the understanding of their advantages and shortcomings, can give you a quick benchmark for property evaluation. Besides, suppose you are familiar with the prevailing interest rate environment and the direction of the monetary policy. In that case, you can more confidently determine what is a good cap rate to apply.

FAQs

What’s a good cap rate for a rental property?

A rule of thumb states that a good cap rate is between 4-12%. However, where on this scale is best for you will depend on how much risk you can deal with. More risk is a higher reward, so a higher cap rate, while for lower risk, the cap rate should be closer to 4%.

Does cap rate include mortgage?

Cap rate does not include mortgage, which allows you to accurately assess the return on investment on a property, helping you find the best deal for you. Including your mortgage will allow you to find the levered yield.

Do cap rates rise with interest rates?

Yes, cap rates rise with interest rates. This relation is because the amount of money you can make investing in government bonds increases, which becomes a more attractive option, increasing the risk of investing in something else.

What does a 7.5 cap rate mean?

A 7.5 cap rate means that you can expect a 7.5% annual gross income on the value of your property or investment. If your property's value is $150,000, a 7.5 cap rate will mean a yearly return of $11,250.