This online sales tax calculator solves multiple problems around the tax imposed on the sale of goods and services. It can calculate the gross price based on the net price and the tax rate, or work the other way around as a reverse sales tax calculator. The sales tax system in the United States is somewhat complicated as the rate is different depending on the state and the base of the tax. If you would like to get more insight into this topic, you can read below to find out about what sales tax is, what is the difference between sales tax and value-added tax, what is its history, how to calculate sales tax and what it looks like in various U.S. states together its economic implications.

How to use the sales tax calculator

Get to grips with our sales tax calculator effortlessly and understand how much tax is added to your purchases or how much a product costs before tax. Just follow these steps:

-

Enter the sales tax rate: In the sales tax field, type in the tax rate percentage that applies to your item.

-

Input the net price: If you know the price before tax, enter this amount in the net price field. This is the price of the product without tax.

-

Calculate the gross price: The calculator will automatically provide you with the gross price, which is the net price plus the sales tax amount.

-

Find the tax amount: It will also calculate the tax amount, showing you exactly how much tax you're paying on the purchase.

This tool is also reversible, meaning:

-

If you know the gross price and want to find out the net price and the tax amount, you can enter the gross price and the sales tax rate, and the calculator will work out the rest.

-

Similarly, if you have the gross price and the tax amount but need to know the tax rate, input these two figures, and the calculator will determine the rate for you.

For example, if you're purchasing a product that costs $100 before tax and there is a 20% sales tax, the calculator will show you that the gross price of the product is $120, with $20 being the amount of tax paid.

Conversely, if you paid $120 for an item and know that the tax amount was $20, the calculator can confirm that the net price was $100 and the sales tax rate was indeed 20%.

Explore further to learn about how sales tax is applied in different regions, the difference between net and gross prices, and how understanding this can benefit your budgeting and financial planning.

Sales tax definition

Sales tax is a consumption-based tax that is indirectly charged on the consumer at the point of final purchase of a good or service. The indirect feature of the tax means that the consumer bears the burden of the tax, however it's collected and transferred to authorities by the seller. The most popular type of sales tax is the retail sales tax which is present on state-level in the United States. Under such a taxation framework, consumers pay the price of the item plus the amount of the sales tax which is collected by the store at the cash register and printed on the receipt. In the next section, you can get more insight into its concept as we illustrate the difference between the sales tax and value-added tax.

Sales tax vs. value-added tax (VAT)

Sales tax can take several different forms: it can be imposed at a single or multiple stages of production or distribution. It can also be levied at the manufacturing level, the wholesale level, or at more than one but less than all levels of production or distribution. Retail sales taxes, which are prevalent in most of the states in the U.S. and are levied by some of the provinces in Canada, is a single-stage tax. It means that the tax obligation emerges only at the point when the sale takes place. In contrast, the value-added tax (VAT) or, under another name, the goods and services tax (GST) is a multi-stage tax imposed on every level of production or distribution chain (from the factory, through wholesalers to retailers). Ultimately, the consumer bears all taxes, since previous participants in the chain deduct the amount of VAT they paid when they made the purchase. It means that each participant in the production chain pays VAT only for the "added value" they create that eventually passed to the final consumer.

In both types of taxes, the tax burden is charged on the final consumer; however, they have a different framework of collection, administration, and effects on the economy. Through a simple example, the below table illustrates the comparison between VAT and retail sales tax. Imagine a lumberjack cutting trees (without cost) who sells the wood (enough for one barrel) to a sawmill owner for $100. The sawmill owner cuts the wood into oak staves and sells it to the cooper for $150. The cooper then makes a barrel that he can sell for $300 to the retailer who eventually sells it to the customer for $350. The total VAT paid is $35 or 10% of the sum of values added at each stage. In the case of retail sales tax with the same 10% rate the paid tax is identical, however, it's assessed only at the point of sale to the customer.

Stage | Product | Price | Value Added | 10% VAT | 10% Retail Sales Tax |

|---|---|---|---|---|---|

1 | log | $100 | $100 | $10 | |

2 | stave | $150 | $50 | $5 | |

3 | barrel | $300 | $150 | $15 | |

4 | barrel | $350 | $50 | $5 | $35 |

Total Tax | $35 | $35 |

The two crucial implications of the difference between retail sales tax and VAT is that retail sales tax is more straightforward and applied on a lower scale of goods and services, therefore it demands lower administrative cost charged on the authorities. However, it also means that the tax burden might be more palpable for the ultimate consumer. Moreover, as you will see in the following, the high diversity of sales tax structures over U.S. states can hurt the economy through distorting consumption and investment.

History of the sales tax

The very first taxes in human history were direct taxes, which are a type of tax imposed on individual persons. The most general ones were the corvée, compulsory labor provided to the state in Egypt (around 2600 BC), and the tithe, where crops and grains were given to the state from landowners, which was invented in ancient Mesopotamia. Sales tax, which belongs to another basic form of taxation, the indirect taxes, were also present in ancient time. Tomb paintings in Egypt, dating back around 2000 BC, portray tax collectors and sales taxes on commodities, such as cooking oil, can be traced to that time (Fox, 2002). In Europe, sales tax appeared firstly during the reign of Julius Caesar around 49 BC-44 BC, when the government of Rome enforced a payment of 1 percent sales tax. Sales tax gradually became widespread over Europe. Spain had a national sales tax from 1342 until the 18th century, with rates varying between 10 and 15 percent. Also, it was introduced in France where it didn't enjoy much popularity: during the 17th century alone, there were 58 rebellions against it (Burg, 2003). However, in modern times the sales tax in Europe took a declining path, and from the 1960s the dominating consumer-based tax steadily became the value-added tax.

Interestingly, the value-added tax appeared first in the academic research of the American economist T. S. Adams in the United States between 1910 and 1921. However, the U.S. Congress only took into consideration the implementation of a federal (nation-wide) sales tax as a source for revenue to finance World War II. Until now, it never passed the conceptual level. Instead, sales taxes are levied and controlled at the state (sub-national) and local (sub-state) levels, where they account for a significant part of state and local revenue.

The use of sales taxes appeared in the U.S in 1821; however, these early taxes were not wide-ranging. The modern retail sales tax emerged during the Great Depression as a response for a massive fall in state revenues. It became the central pillar of state fiscal system through the second half of 20th century. At the moment, 5 of the 50 US states are without a sales tax: Alaska, Delaware, Montana, New Hampshire, and Oregon.

How to calculate sales tax with our online sales tax calculator

- Find out the sales tax rate. In our example, let us make it

4%. - Find out the net price of a product. Let's use

45. - Multiply your net price by 4%, so by

0.04, to find out the tax amount:45 * 0.04 = 1.8. - Add the tax amount to the net price to find out the gross price:

45 + 1.8 = 46.8.

As you can see, this is precisely the same as how you calculate percent increase... or if you want to find out the pre-tax price while using our calculator, simply input the gross price and the sales tax rate to perform the reverse sales tax calculation!

Besides, it's quite likely that you'll find our margin calculator or the margin with sales tax calculator handy as well, especially if your job is in any way related to sales.

Sales tax in the United States

As mentioned before, most of the states in the U.S. apply a single-stage retail sales tax with different rates and scopes: there are 46 different sales taxes with distinct exclusions. As Schenk and Oldman (2007) pointed out, the relatively high diversity in the enacted tax law in various states have several economic implications:

- Business conducted on a nation-wide scale need to devote substantial resources to comply with many states and local sales taxes. It increases the complexity and administrative costs related to businesses.

- As most of the services are not subject of sales taxes, the total tax base is shrinking due to the expanding trend of electronic services (for example Amazon or eBay) and the increase in the sharing economy (for instance Uber or Airbnb).

- Tax evasion is expanding as the current sales tax system inefficiently tax most cross-border and mail order shopping by consumers.

These issues become more relevant if we take into consideration the significant contribution of sales taxes to state revenues and the current transformation of the economy. It is not surprising then that recent studies have begun to address these problems and examine the possibility of a nation-wide introduced federal VAT or another consumption-based tax which may coexist with the state-level sales tax.

Another alternative direction that achieved stronger political response is the harmonization of the current sales taxes, which is an ongoing challenge: an early stage of sales tax adjustments began in October 2005, with the implementation of a Streamlined Sales Tax. In brief, each state which joins the agreement must fulfill several conditions aimed at enhancing unification and simplifying taxation between members. The most crucial requirements are the following:

- Each participant shall establish a central state administration for all of its state and local sales taxes.

- Each party must adopt a uniform sales tax definition of key terms and a uniform tax base.

- A state can have only one general sales tax rate.

- State authorities shall maintain a comprehensive database together with a central, electronic registration system for all member states.

Today, 24 states have adopted the simplification measures in the Agreement (representing over 31 percent of the population), and more states are moving to accept the simplification measures. For more details and up-to-date information, you may have a look at the official website of .

Economic implications

Besides the specific nature of the sales tax system having an adverse impact on businesses in the U.S., a consumption-based tax, in general, can have multiple economic implications affecting the real Gross Domestic Product (GDP) of a country.

- It may distort saving behavior

Economists, as commonly in a wide range of economic issues, often disagree on the implications of various tax burdens. The discussion on the choice between income tax and consumption tax constitutes one of the heated topics. In the United States, personal income taxes have traditionally played the central role in the federal level, compared to the European countries, where consumption taxes reserve the highest portion of government incomes. There have been several attempts to move the US taxation system towards a consumption-based system as advocates of such a shift argue that it would encourage individuals to save more. The logic behind this debate is that income tax appears on your payslip as a reduction of your salary, thus eventually you have less money that you could devote for savings. On the other hand, a consumption tax emerges only when saving is spent; hence it doesn't alter saving decisions. Since higher savings contribute to higher investment, relying more on consumption tax may favor a higher rate of economic growth.

To address this concern, American policymakers adjusted the income tax law to compensate for such an adverse effect. Taxpayers can settle a limited amount on a special saving account (for example Individual Retirement Accounts and 401(k) plans) that is not subject to taxation until they withdraw their money during retirement. In such a case, people who save through these accounts eventually taxed based on their consumption rather than their income.

- It redistributes income in the economy

Strongly connected to the argument of saving behavior, tax laws which promote savings also impose more substantial weight on people with lower income. It is so because lower-income families usually can't afford savings and they tend to spend all their income on daily consumption, mostly on food; thus such a system reduces the tax burden on wealthier people and pushes the government to impose a higher tax on the poor. It follows that in states where sales tax rates are high, it may widen the gap between rich and poor, thus increasing inequality in the society. Many states as you will see in the table below apply reduced tax rates on foods to ameliorate such adverse effect and help the poor and support families.

- It can alter price levels

Implementation or adjustment of a sales tax rate affects price level, though its magnitude and lasting effect depends on not only the design of the tax law but also the economic factors and the reaction of consumers and sellers to such a change. To see this, let's consider a rise in the sales tax rate in a state. The immediate effect of the change is certainly an increase in price levels of products that are subject of the tax; however, its inflationary effect may be mitigated if the seller doesn't transfer such a cost entirely to the final customer. Such a situation may happen in sectors where the competition is high among sellers, or the consumer demand is more sensitive to price changes. In other words, the full price effect depends largely on the price elasticity of demand. However, even if an altered tax rate brings change in the price level, the duration of the effect is rather short and hardly induce a sustained increase in the inflation rate.

Take a look at our price elasticity of demand calculator to keep reading about this subject.

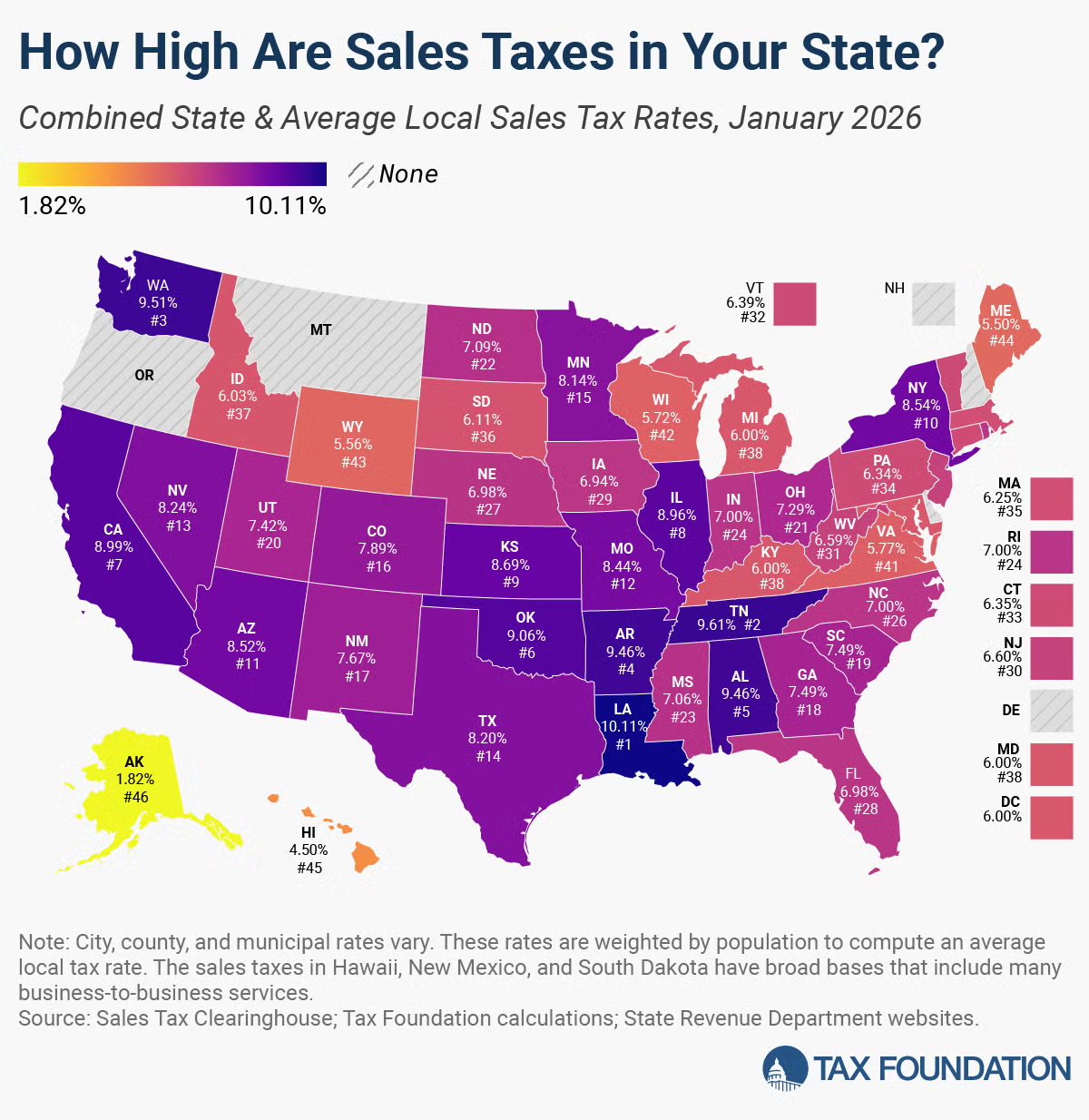

Combined State and Local Sales Tax Rates

The high diversity of state sales tax structures means that states differ in their attractiveness to businesses. There are two key reasons behind it:

- Higher rates and a more complex taxation system raise the cost of production,

- As a response to higher sales tax rates, consumers may reduce consumption or move their shopping to states where the tax burden is low.

An optimal sales tax is one that is applied to a broad base of goods and services with a low tax rate. Such a tax system can minimize adverse impacts, especially economic distortion, that occur when consumers adjust their consumption behavior in response to tax differentials.

The graph below shows the ranking of states by their Combined State and Local Sales Tax Rates in 2026, providing an overview of how attractive tax systems are across the United States.

Sales tax by states in 2026

To demonstrate the diversity of sales taxes in the United States, you can find more details about the applied sales taxes in U.S. states in the following table. Besides, you can check when the different states introduced the sales tax and if there is an exemption or reduced rate on sales of food.

State | State Tax Rate | Avg. Local Tax Rate | Combined Rate | Max Local Tax Rate |

|---|---|---|---|---|

Alabama | 4% | 5% | 9% | 11% |

Alaska | 0% | 2% | 2% | 8% |

Arizona | 6% | 3% | 9% | 5% |

Arkansas | 7% | 3% | 9% | 6% |

California | 7% | 2% | 9% | 5% |

Colorado | 3% | 5% | 8% | 9% |

Connecticut | 6% | 0% | 6% | 0% |

Delaware | 0% | 0% | 0% | 0% |

Florida | 6% | 1% | 7% | 2% |

Georgia | 4% | 3% | 7% | 5% |

Hawaii | 4% | 1% | 4% | 1% |

Idaho | 6% | 0% | 6% | 3% |

Illinois | 6% | 3% | 9% | 5% |

Indiana | 7% | 0% | 7% | 0% |

Iowa | 6% | 1% | 7% | 2% |

Kansas | 7% | 2% | 9% | 4% |

Kentucky | 6% | 0% | 6% | 0% |

Louisiana | 5% | 5% | 10% | 7% |

Maine | 6% | 0% | 6% | 0% |

Maryland | 6% | 0% | 6% | 0% |

Massachusetts | 6% | 0% | 6% | 0% |

Michigan | 6% | 0% | 6% | 0% |

Minnesota | 7% | 1% | 8% | 3% |

Mississippi | 7% | 0% | 7% | 1% |

Missouri | 4% | 4% | 8% | 6% |

Montana | 0% | 0% | 0% | 0% |

Nebraska | 6% | 1% | 7% | 2% |

Nevada | 7% | 1% | 8% | 2% |

New Hampshire | 0% | 0% | 0% | 0% |

New Jersey | 7% | 0% | 7% | 3% |

New Mexico | 5% | 3% | 8% | 5% |

New York | 4% | 5% | 9% | 5% |

North Carolina | 5% | 2% | 7% | 3% |

North Dakota | 5% | 2% | 7% | 4% |

Ohio | 6% | 2% | 7% | 2% |

Oklahoma | 5% | 5% | 9% | 7% |

Oregon | 0% | 0% | 0% | 0% |

Pennsylvania | 6% | 0% | 6% | 2% |

Rhode Island | 7% | 0% | 7% | 0% |

South Carolina | 6% | 1% | 7% | 3% |

South Dakota | 4% | 2% | 6% | 5% |

Tennessee | 7% | 3% | 10% | 3% |

Texas | 6% | 2% | 8% | 2% |

Utah | 6% | 1% | 7% | 5% |

Vermont | 6% | 0% | 6% | 1% |

Virginia | 5% | 0% | 6% | 3% |

Washington | 7% | 3% | 10% | 4% |

West Virginia | 6% | 1% | 7% | 1% |

Wisconsin | 5% | 1% | 6% | 3% |

Wyoming | 4% | 2% | 6% | 3% |

District of Columbia | 6% | 0% | 6% | 0% |

* City, county and municipal rates vary. These rates are weighted by population to compute an average local tax rate.

Source: Sales Tax Clearinghouse; Tax Foundation calculations; State Revenue Department websites.

Sales tax deduction

Paying sales taxes can be a chore, especially if you are about to buy an expensive product, for example, a car. However, there might be a way to reduce your tax burden. There are two ways to gain some tax advantage: either you deduct state and local general sales tax you paid during the year, or you may deduct the state, local and foreign income tax you paid during the year. You can't do both, and there are also some limitations. To decide which way is better for you, as a general rule, compare the amount of sales tax you paid in the year to the amount of the state, local and foreign income tax paid in the year. Then deduct the larger of the two amounts.

If you choose to deduct your sales tax, you have two options for the procedure:

- You may keep all bills and invoices of your actual sales tax expenses, or

- You can estimate the amount of tax you paid by, for instance, using the .

If you would like to know more details you may visit the official site of the where you can find all relevant information on this topic.

Behind the scenes of the sales tax calculator

Tibor, a PhD in Statistical Methods in Economics, is the mastermind behind the sales tax calculator.

This calculator's genesis occurred as Tibor navigated the labyrinth of sales tax implications on business models and consumer purchases. He realized the necessity for a tool that could elucidate the direct financial impact of sales tax on both net and gross prices, leading to the creation of this calculator.

This tool is invaluable for individuals trying to decipher the true cost of products post-tax and for businesses aiming to communicate pricing to customers transparently. Tibor relies on this calculator to assess the tax implications for new product launches and keep abreast of financial analytics.

You can trust this sales tax calculator because we are committed to accuracy and reliability. Each feature is meticulously peer-reviewed by experts in finance and tax regulations, and the content is carefully proofread to ensure clarity and precision. Please refer to our Editorial Policies page for further details on our editorial standards.

FAQs

What states don’t have sales tax?

Alaska, Delaware, Montana, New Hampshire and Oregon all do not have a statewide sales tax, although Alaska and Montana both allow local sales taxes. Delaware also imposes a gross receipts tax on businesses. Some other states have not taxes on food and other items.

How is an excise tax different from a sales tax?

An excise tax is a tax on specific goods and services, usually those considered harmful, while a sales tax is a general tax on most things. Excise taxes can also be per unit (e.g. per bottle of alcohol), while sales taxes are always as a percentage of the item’s cost.

Do I charge sales tax for out of state customers?

In most cases, you do not charge sales tax on an out of state order. If an out of state customer comes to your state to make the purchase, you can collect tax on that. You should, however, consult your local law, as your area may be different.

How do I calculate sales tax backwards from the total?

- Subtract the net price from the gross price to get the tax amount.

- Divide the tax amount by the net price.

- Multiply the result of step 2 by 100. The result is the sales tax.

How much is sales tax on a car?

Sales tax on a car is the same as the sales tax throughout the rest of the state. Certain cities and regions within a state may also have additional sales tax. When in doubt, check your local area for all of the information.

Do you pay sales tax on a house?

There are taxes to be paid when purchasing a house, but they are not sales tax. Instead, these are the property and transfer tax. Please check your local laws for more information regarding these taxes.

Is sales tax regressive?

Yes, sales taxes are regressive. They are charged as a percentage of the sale price, and therefore are the same regardless of your income. This means that a poorer person pays a larger percent of their income.