The deferred annuity calculator (also the deferred income annuity calculator or deferred life annuity calculator) is a handy tool to answer three important questions that may arise when you are thinking about investing in a deferred annuity:

- How much money will I have when I retire?

- How much money can I withdraw?

- How long will my annuity last?

Read on where we explain the deferred annuity definition by showing you the main differences between immediate and deferred annuities as well as some deferred annuity examples. Moreover, you can learn the deferred annuity formula and what is a tax-deferred annuity.

If you are more interested in a specific retirement plan, check our 401k calculator. Or, if you would like to learn more about annuities in general, check our annuity calculator, where we provide you with high flexibility in the computations.

What is a deferred annuity — the deferred annuity definition

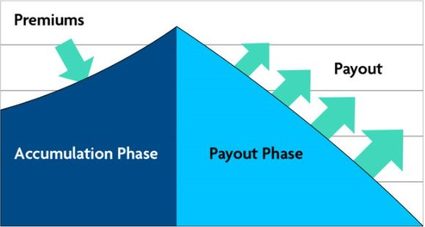

A deferred annuity is an insurance contract in which the annuity provider agrees to transfer you a regular income or a lump sum of money at some date in the future. Deferred annuities have an accumulation phase where you can add funds to your annuity account. The interest is deferred until the end of the accumulation phase.

The second part of the deferred annuity is the payout phase where you can receive withdrawals.

There are different types of deferred annuities:

-

Fixed deferred annuity

A fixed deferred annuity works similarly to a certificate of deposit (CD). Instead of having to claim the interest gains on your tax return each year, though, the interest is deferred until the payout phase. -

Variable deferred annuity

When you buy a variable deferred annuity, your funds are put into an investment account. You can choose how the funds are invested based on your risk tolerance and other factors. -

Equity-indexed annuity

It's a type of fixed annuity, but its return comes from two sources: a minimum guaranteed interest return and a sum linked to an equity index. The sum from the equity index is based on the performance of a particular stock market index, such as the S&P 500 Index. In this way, you can earn a percentage of the index's growth (participation rate). For example, if the S&P 500 grew by 10 percent in a year and you have a 50 percent participation rate, you would earn 5 percent interest. -

Longevity annuity

This works as a long life expectancy insurance. A deferred annuity example, in this case, would be depositing 100,000 dollars into a longevity annuity at age 70. The insurance company would then guarantee you an agreed amount of withdrawals for the rest of your life starting at age 80.

Note that the present calculator functions as a fixed deferred annuity. You can also use it to build a tax-deferred annuity plan (TDA or 403b), a type of retirement plan designed to complement your employer's base retirement plan.

What distinguishes a deferred annuity from an immediate annuity?

The main difference between immediate and deferred annuities is that an immediate annuity's payments begin almost immediately, but with a deferred annuities, payments are delayed. During that time, any earnings in the account are tax-deferred.

In other words, an immediate annuity starts paying out as soon as you make a lump-sum payment to the insurer. In contrast, a deferred annuity begins its payments on a specified future date.

The deferred annuity formula

The best way to represent the deferred annuity formula is to divide it into two parts:

- Accumulation phase (future value of annuity due)

where:

- or Future Value — Final balance will be the initial balance (PV) at the beginning of the payout phase;

- — Regular payment;

- — Annual interest rate (in decimal form); and

- — Number of years until the end of the accumulation phase.

- Payout phase

where:

- — Regular withdrawal, i.e., the amount you take out each month;

- or Present Value — Initial balance or principal;

- — Annual interest rate (in decimal form);

- — Number of compounding periods in one year; and

- — Number of years you plan to make withdrawals.

How to use the deferred annuity calculator

Now that you know what a deferred annuity is, let's see how to use our deferred annuity calculator:

1. Select what you would like to know:

- How much can I withdraw?

- How long will my annuity last?

2. Provide information about the deferral (accumulation) phase:

- Choose the way you would like to determine the length of the accumulation phase.

- Provide a lump sum payment. This will be the opening balance at the beginning of the annuity accumulation phase.

- Input a monthly contribution if you plan to make a regular deposit before the withdrawals.

- Find the expected rate of return. This is the average interest rate or rate of return during the accumulation phase. If you want to learn more about it, check our rate of return calculator.

By ticking the Show advanced settings checkbox, you'll find:

- Timing of contribution — Here you may set annuity due (payment at the beginning of periods) or ordinary annuity (payment at the end of periods).

- Growth rate of contribution — The percentage growth rate of your contribution over a year.

- Monthly growth rate — The percentage growth rate of the monthly contributions. Note that periodic and annual growth rates are linked together: if you set one, the other will be calculated according to annuity frequency. Available only in the fixed-length annuity mode.

3. Payout phase (for withdrawals)

- Length of withdrawals - Set the term of the planned withdrawals.

- Withdrawal frequency - Interval between the regular withdrawals.

- Expected rate of return - The average interest rate or rate of return during the payout phase.

Advanced payout phase settings:

- Timing of contribution.

- Growth rate of withdrawals.

- Periodic growth rate.

- Compounding method — The frequency of adding interest to your balance. Note that it applies over the whole lifetime of the annuity.

4. Results

After setting the above parameters, you can immediately read the main results and see a summary table with all the additional information.

Disclaimer

You should consider the deferred annuity calculator as a model for financial approximation. All payment figures, balances, and interest figures are estimates based on the data you provided in the specifications that are, despite our best effort, not exhaustive.

For this reason, we created the calculator for instructional purposes only. Still, if you experience a relevant drawback or encounter any inaccuracy, we are always pleased to receive useful feedback and advice.