Table of contents

Survey: Most Americans Have Financial Regrets for 2025

Report Highlights

- 8 in 10 Americans (80%) have financial regrets for 2025.

- Overspending on non-essentials is the top financial misstep, cited by 29%.

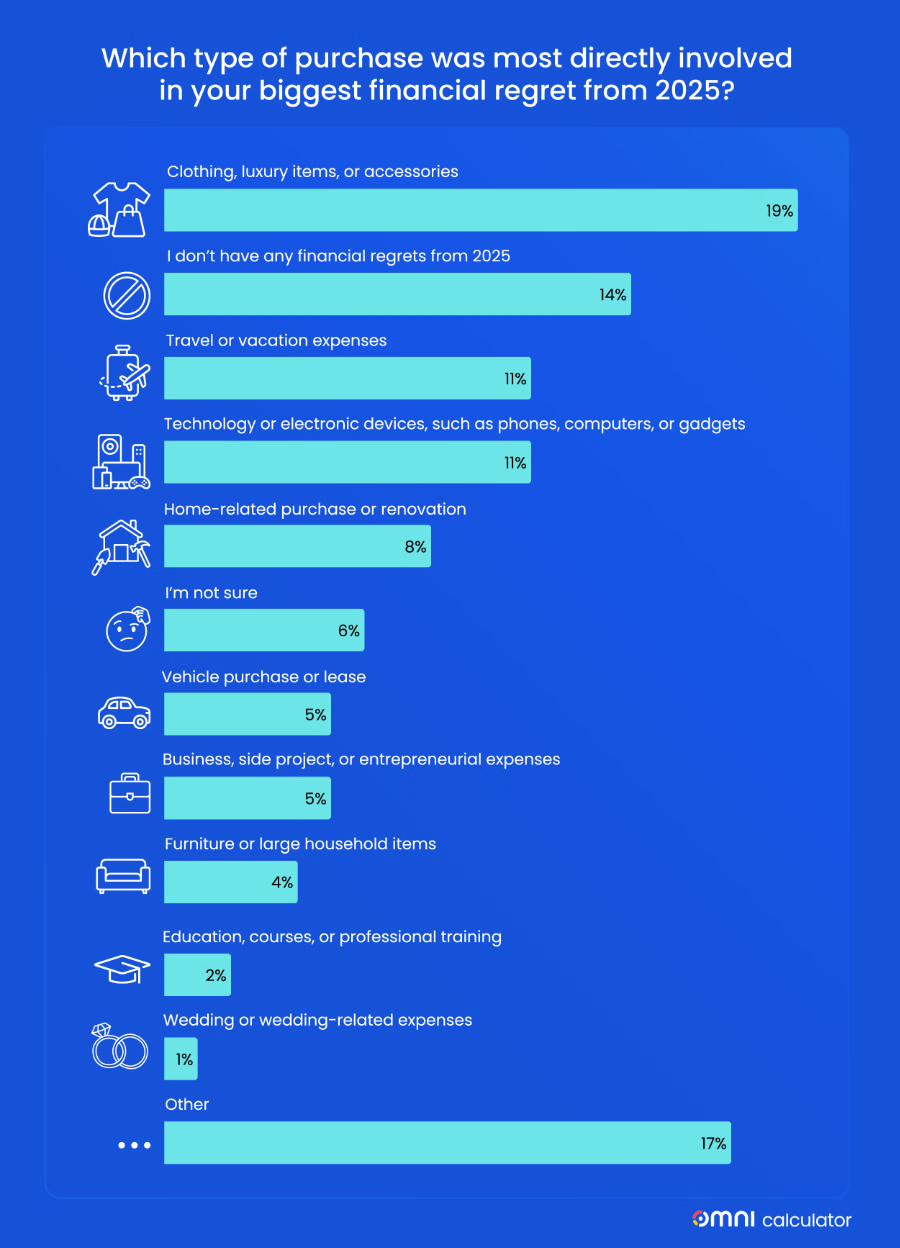

- Clothing, luxury items, or accessories (19%) lead regret-linked categories, followed by travel or vacation expenses (11%) and technology/electronic devices (11%).

- Rushed decisions, without enough planning (28%), were the leading cause of financial mistakes.

- Some 31% say a higher income, such as a raise, promotion, or additional work, would most improve their finances in the next 6-12 months.

With 2026 underway, many Americans are reflecting on their financial decisions from 2025.

This new survey from Omni Calculator examines how often financial regret occurs, what decisions lead to it, how much it costs, and more.

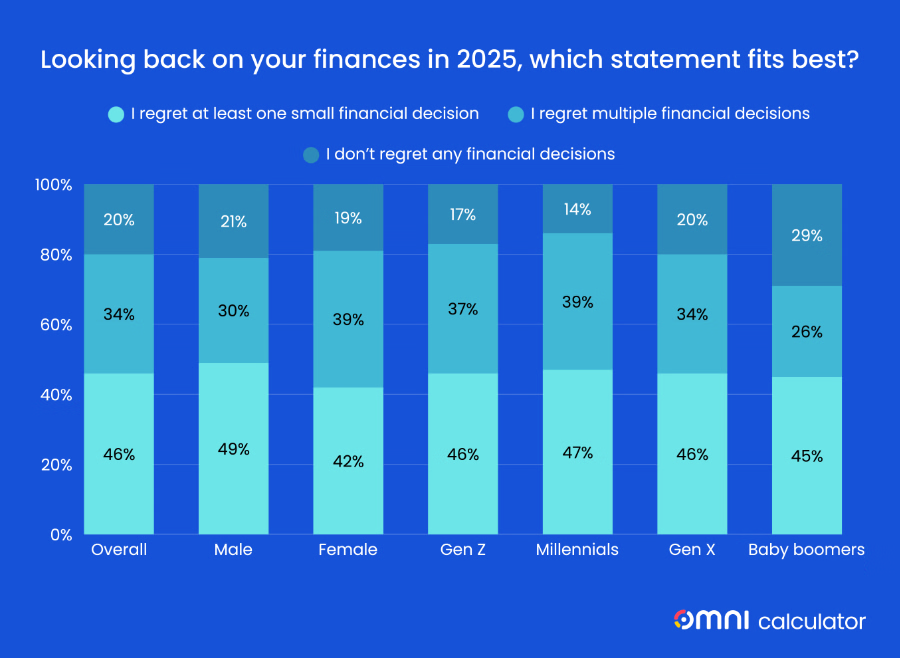

A majority of respondents reported some level of financial regret.

Overall, 46% say they regret at least one small financial decision, while 34% report multiple financial missteps.

By gender, 49% of men report at least one small regret compared with 42% of women, while multiple regrets are more common among women at 39% vs. 30% of men.

Across generations, single small regrets are consistent, at 47% among millennials, 46% among Gen Z and Gen X, and 45% among baby boomers. Multiple regrets are highest among millennials at 39%, followed by Gen Z at 37% and Gen X at 34%, while baby boomers report the lowest rate at 26%.

One in five adults (20%) report no financial regrets for 2025, with baby boomers leading the way (29%).

When asked which type of purchase was most directly involved in their biggest financial mistake, 19% point to clothing, luxury items, or accessories, followed by 11% for travel or vacation expenses, and 11% for technology or electronic devices such as phones, computers, or gadgets.

Another 8% point to home-related purchases or renovations, 5% report vehicle purchases or leases, and 5% identify business or entrepreneurial expenses. In comparison, 4% reference furniture or large household items, 2% point to education or professional training, and only 1% report wedding-related expenses.

A substantial 17% selected “Other”, which allowed respondents to write in their own answers.

Responses in this category often reference food and dining, including fast food, delivery, and restaurants; entertainment and lifestyle expenses such as gambling, gaming, alcohol, and social events; seasonal spending such as holiday gifts; financial support to friends or family; taxes, legal fees, and investment decisions; medical, veterinary, and car repair costs; and, in some cases, a lack of saving rather than a specific purchase.

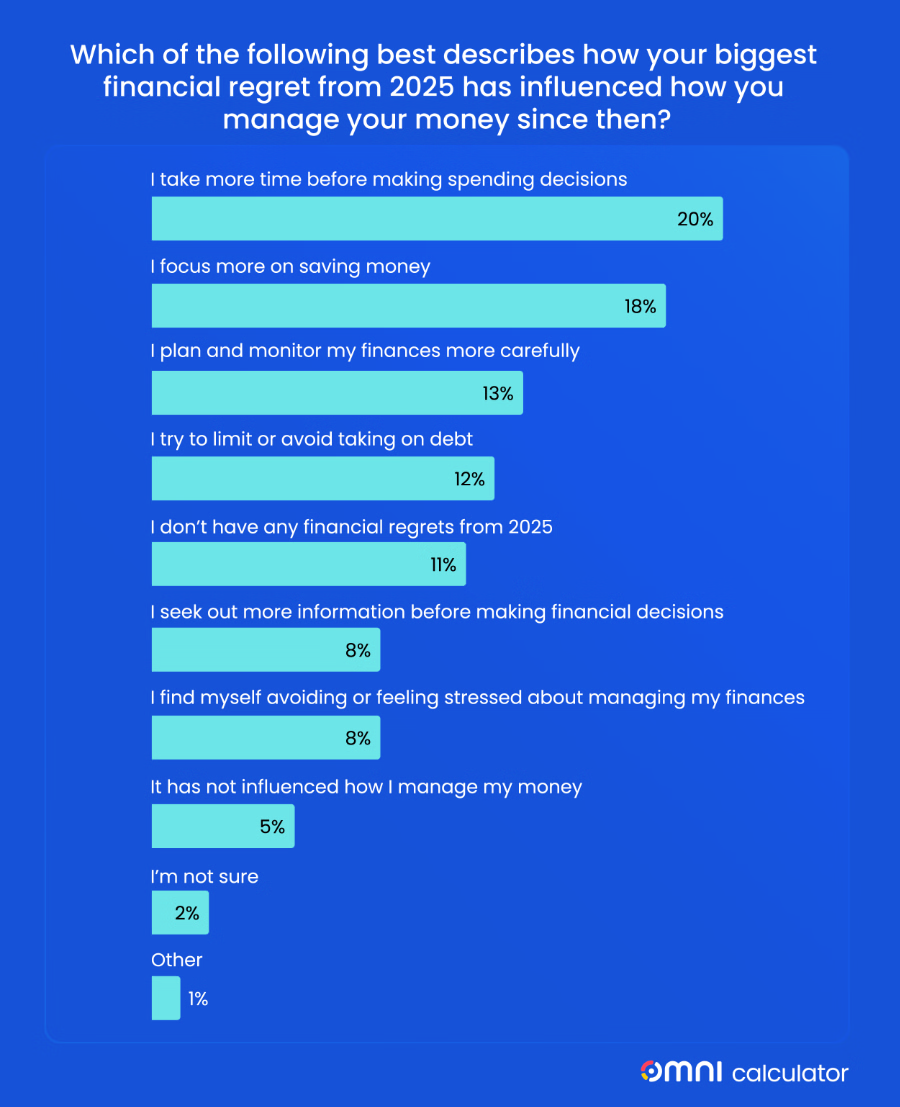

Many respondents report changes in how they manage money after their biggest financial misstep in 2025, with 20% of Americans now taking more time before making spending decisions.

An additional 18% mentioned a stronger focus on saving, while 13% said they plan and monitor their finances more carefully. Another 12% indicated they now try to limit or avoid taking on debt.

Behavioral adjustments also included 8% seeking more information before making financial decisions, and another 8% reporting increased avoidance or stress around managing finances. A smaller share said their approach didn’t change (5%).

To gather additional context on how these mindset shifts translate into personal advice, respondents answered an open-ended question: “If you could give one piece of financial advice to your 2025 self, what would it be?”

The most common advice was to save more, especially by building an emergency fund and setting money aside consistently, followed by guidance to slow down spending, wait before making purchases, and separate wants from needs. Many responses also stressed better research before major expenses, including vetting contractors, comparing quotes, and reading reviews, alongside stronger debt control, such as avoiding credit card balances and limiting high-interest debt.

Structured planning appeared often, including budgeting, planning large expenses, and staying focused on long-term goals, with additional mentions of investing earlier, seeking professional advice, negotiating pay, and increasing income.