The mortgage prepayment calculator estimates the impact of making extra payments on your mortgage loan amount, the loan's term, and its accruing interest. Prepayment means paying off your mortgage faster than the schedule to do so. Although it seems like a financially and even emotionally beneficial thing to do, disrupting your repayment schedule sometimes has unforeseen implications that could make the decision unfavorable.

The mortgage prepayment calculator will help you figure out if you will save more or incur more costs in the long term by paying off your loan faster. Therefore, this calculator can also be used as a mortgage acceleration calculator.

This article will explain how mortgage prepayment works, the mortgage prepayment penalty, and alternatives you can explore to pay off your mortgage smartly. For instance, increasing the frequency of your mortgage payments, such as the biweekly mortgage payment schedule, can lead you to make 13 months of mortgage payments in a year, compared with the regular 12 months. You can estimate the prepayment penalty and learn how to reduce or even avoid them completely using our mortgage penalty calculator. You may want to look up the FHA and VA loans which have no prepayment penalty.

What is mortgage prepayment?

Mortgage prepayment means that you pay all or part of the money owed on your mortgage before it’s officially due. You can prepay a mortgage loan if:

-

You find a cheaper interest rate and want to take advantage of it by refinancing. Refinancing means that you take a new mortgage loan with a cheaper interest rate to pay off the old costlier one. Mortgage interest rates can become cheaper if market interest rates decline or your creditworthiness improves over time for lenders to consider offering you a favorable interest rate. Take a look at our mortgage refinance calculator if you are interested.

-

The loan balance or the principal amount left on the mortgage loan is relatively small, and you have enough to settle the remainder early. This type of prepayment can happen when you’ve been servicing the loan for a considerable time. As time passes and you gain more equity on the property with your monthly payments, the principal amount gets smaller.

-

Your income improves significantly compared with when you first took the mortgage loan. A lot can happen over a mortgage term that can affect your ability or desire to pay off your mortgage sooner than you had initially anticipated. Your financial condition can be different in a few years or even tomorrow if you receive a windfall, a better salary, or a bonus, it only makes sense to clear all or some of your debts.

Whatever the case, by paying what you owe early, you can cut down the amount of interest you owe to the lender and the duration of your mortgage loan.

Ways you can prepay mortgage

You can prepay your mortgage by paying a lump sum or making small extra payments on your regular monthly installments. These additional payments are deducted from the principal balance, which reduces the total amount of interest the loan would have accrued to the lender.

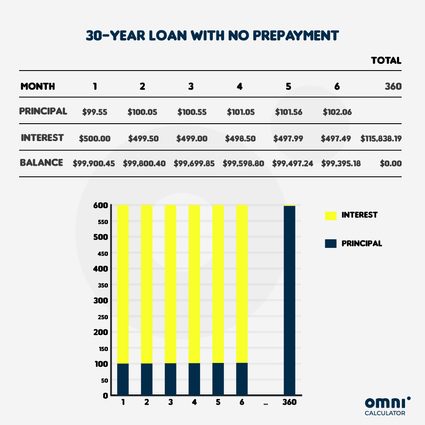

For instance, if you take a $100,000 mortgage loan at a fixed interest rate of 6% each year for 30 years, you will be expected to repay a portion of the $100,000, and interest of 6% / 12 = 0.5% each month for 30 × 12 = 360 months until you pay off the loan or principal.

monthly payment = portion of principal + interest for the month

By spreading out or amortizing your loan payments, the lender calculates interest based on the principal balance at the beginning of each compounding period. Usually, mortgage loans are compounded monthly, so the interest you pay is calculated on the principal balance at the beginning of each month during the loan term. The interest for the month is calculated using the formula:

interest = interest rate × principal balance

where:

principal balance = principal - the portion of principal paid off

If you use our mortgage calculator to determine how much is expected of you to pay monthly, you will find that the fixed monthly payment to cover the loan is $599.55.

Therefore,

For the first-month payment:

The interest you pay is:

= 0.5% × ($100,000 - $0) = $500

While the portion of principal paid off is:

= $599.55 - $500 = $99.55

The principal balance at the end of the first month is

= $100,000 - $99.55 = $99,900.45

For the second-month payment:

The interest you pay will be:

= 0.5% × $99,900.45 = $499.50

The portion of principal paid off is:

= $599.55 - $499.50 = $100.05

And the principal balance at the end of the second month is:

= $99,900.45 - $100.05 = $99,800.40

If you maintain the scheduled payments, your monthly installments in the first 6 months will look like this:

Thus, the interest portion of the monthly payment decreases every month as you pay off more principal.

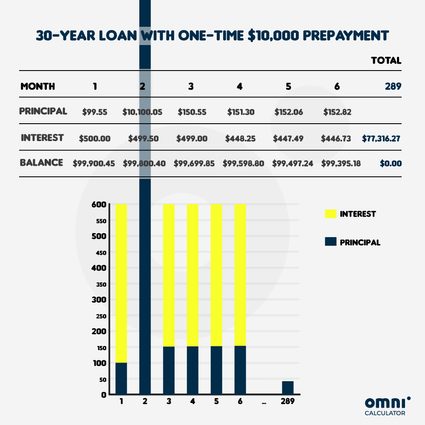

One-time Lump sum prepayment

Now, suppose you decided to pay off $10,000 along with your monthly installment in the second month after collecting a bonus at work or winning a lottery, for instance. In that case, you will save $50 in interest payment on your third month, but reduce your total interest paid by $38,522.92, and the number of monthly payments you should've made to 289 from 360.

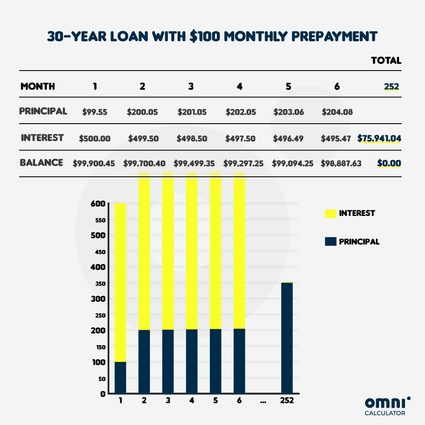

Extra monthly payments

However, if you decided that you’ll make an extra payment of $100 on your monthly installments instead, you can save even more:

How to use the mortgage prepayment calculator

Using the mortgage prepayment calculator, you can easily compare each prepayment's outcome – both periodic and lump sum prepayments – in the prepayment summary table. All you have to do is provide the information on your mortgage plan in the following simple steps:

-

Input the

Mortgage amount, which is the value of your original mortgage or the remaining loan principal you have to repay. -

Provide the

Interest rateandLoan term. -

Select the

Interest rate calculation method. Most countries use a monthly compounding interest rate, while some countries like Canada compound the interests annually. -

Provide your next mortgage

Payment due date. Pick the date upon which your mortgage payments are due. -

Select how frequently you make payments from the

Payment frequencydropdown list. -

If you want to make periodic prepayments, e.g., $100 monthly prepayments, then input the value into the:

-

Periodic prepaymentfield, and indicate the date you want toStart from; if you do not want to make any periodic prepayments -

You can choose to find out the result of making a one-time

Lump sum prepaymentby inputting the amount you want to prepay, e.g., $10,000, and selecting a date in thePaid onfield to indicate when you want to make this prepayment.

You can even input values for both fields to determine how making both periodic and lump sum prepayments can change your mortgage loan outcome in different scenarios.

As you input these values, the calculator automatically evaluates your mortgage loan impact and provides you with results to compare the scenarios in the prepayment summary table. For an in-depth review of these results, you can check out the chart of balances and table of payment schedules to see how exactly you chip off those mortgage balances with each payment!

-

Whenever you make an extra payment on your loan, you reduce your outstanding principal amount. All future interest payments will be lower because they are calculated based on a lower outstanding loan balance. In the end, you shorten the loan term and pay it off faster.

Mortgage prepayments benefit borrowers by reducing their:

- Outstanding balance of the loan;

- All future interest payments; and

- The duration of the mortgage loan.

But they rarely benefit the mortgage lenders; hence, they charge a mortgage prepayment penalty.

What is mortgage prepayment penalty?

Mortgage lenders have a love-hate relationship with prepayments. On the one hand, they’re glad a borrower did not default on the loan payment, but on the other hand, they have to forgo the interest they would have gained if the borrower had stuck to the original loan agreement. Furthermore, lenders insure mortgage loans by offering them as a bond to investors who are paid with some of the interest on the loan. So if a loan is prepaid and the interest is less, they rarely profit. That is why most lenders often include a prepayment charge or penalty clause in the mortgage loan contract to compensate for the economic costs.

A mortgage prepayment penalty is an agreement between a borrower and a bank or mortgage lender regulating what the borrower can pay off and when.

Different types of mortgage loans

Most mortgage lenders try to balance the effect of prepayments on their bottom line by offering:

-

Different types of mortgage loans, such as the open-end mortgage and the closed mortgage.

-

Open end mortgage with a high-interest rate but no restrictions on how much or when you can pay off the loan;

-

Variable-rate closed mortgage with fluctuating interest rates but a fixed prepayment charge; and

-

Fixed-rate closed mortgage, with generally strict conditions and prepayment charged based on how long you’ve held the mortgage loan. For example, the prepayment penalty may be higher if you pay off your loan in 1 year than if you pay it off in 2 years.

-

- Prepayment privileges that allow borrowers to pay off up to 20% of a loan balance each year. Or increase mortgage payments by up to 20% once each year. But when the prepayment amount exceeds the prepayment privilege permitted under the mortgage contract, the charges kick in. You can determine the exact point where the extra charges kick in with the mortgage prepayment calculator.

Generally, a mortgage prepayment penalty is designed for the following reasons:

- To make the loan interest rate cheap and attractive;

- Discourage borrowers from refinancing, selling the home during the mortgage term, or paying off the loan too early;

- Stop the transfer of a mortgage to another lender; and

- Provide compensation for mortgage bond investors.

Different lenders offer different prepayment terms, so you must ask that the terms are explained adequately before closing a mortgage contract.

Pros of mortgage prepayment

- You pay less money in interest, and you pay off your mortgage faster.

- If you have other investments that generate return less than the interest rate you pay on your mortgage, prepaying your mortgage will help you save money.

- The interest on your mortgage is tax-deductible. However, if you were investing the same money elsewhere, you’d be paying taxes on the income.

- You become a homeowner sooner by increasing your equity on the home with prepayments.

Cons of mortgage prepayment

- Prepaying your mortgage may end up costing you more if you factor in the prepayment penalty and other fees for closing the mortgage, which can make paying off your mortgage faster, actually costlier.

- You will have fewer funds for other needs when you commit to prepaying your mortgage. So, if your monthly income is not sure, you might be in a difficult situation when an emergency expense arises.

- Inflation can reduce the real value of your fixed-rate mortgage over time. Prepaying your mortgage instead of investing in safe investment options – such as the fixed deposit or a recurring deposit account – with a shorter relative term to your mortgage means that you lose money in the long-run.

- Mortgage interest payments are tax-deductible. You lose the chance to save money in taxes when you prepay because the interest expense you can deduct from your taxes declines.

Conclusion

In conclusion, it is best to always factor in prepayment provisions for a mortgage loan and weigh the benefit of prepaying to the fee you have to pay before taking one. The rule of thumb is that:

-

If a mortgage is accruing lesser interest than the return you can gain from other investment options, don’t prepay.

-

If you anticipate you'll prepay, take out mortgage loans with lower principal balance and higher interest rates instead of loans with higher principal balance and below-market-rate interest, which is best for people who don’t intend to prepay.

-

Lastly, if you decide to prepay because your goal is to own your home faster, i.e., you're using this mortgage prepayment calculator as a mortgage acceleration calculator, then make sure you confirm with your mortgage lender that the prepayments go towards your mortgage principal balance.

Disclaimer

You should consider the mortgage prepayment calculator as a model for financial approximation. All payment figures, balances, and interest figures are estimates are based on the data you provided in the specifications that are, despite our best effort, not exhaustive.

For this reason, we created the calculator for instructional purposes only. Yet, if you experience a relevant drawback or encounter any inaccuracy, we are always pleased to receive useful feedback and advice.